How to Create the Next Facebook: Seeing Your Startup Through, From Idea to IPO (17 page)

Read How to Create the Next Facebook: Seeing Your Startup Through, From Idea to IPO Online

Authors: Tom Taulli

There are many flaws with the PE ratio, though. Perhaps the biggest is that it’s backward-looking: it’s based on the past 12 months of earnings. So, investors may instead use a forward PE ratio:

Price / Earnings Forecast for the Next 12 Months

And if a company has losses—which is common for tech companies—then these metrics are meaningless. What to do? Investors instead often look at the price-to-sales ratio:

Market Capitalization / Sales

The

market capitalization

(or

market cap

) is the stock price times the number of shares outstanding. It’s essentially the total value of the company.

The price-to-sale ratio is a good way to compare the value of one company to another. For example, if Groupon has a ratio of 5 and LivingSocial’s is 3, then Groupon is commanding a premium valuation.

Of course, Wall Street looks at other metrics as well. But for the most part, they focus on earnings and revenue growth. Because of this, a publicly traded tech company often announces its earnings and revenue forecasts for the next quarter and the full year. This helps to reduce volatility in the stock price because investors have a better sense of the company’s momentum. Wall Street hates surprises.

But some companies like Facebook and Google don’t provide any guidance. Their belief is that they should be focused on long-term growth, not quarter-by-quarter results. This approach is fairly rare on Wall Street; only marquee companies can do it.

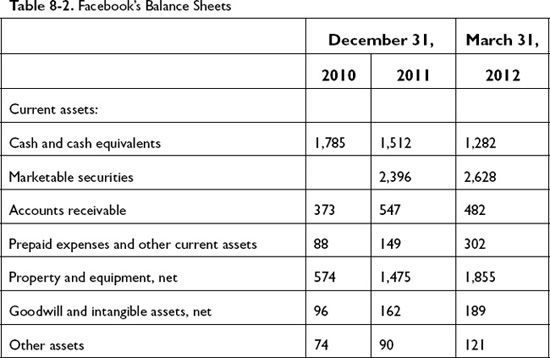

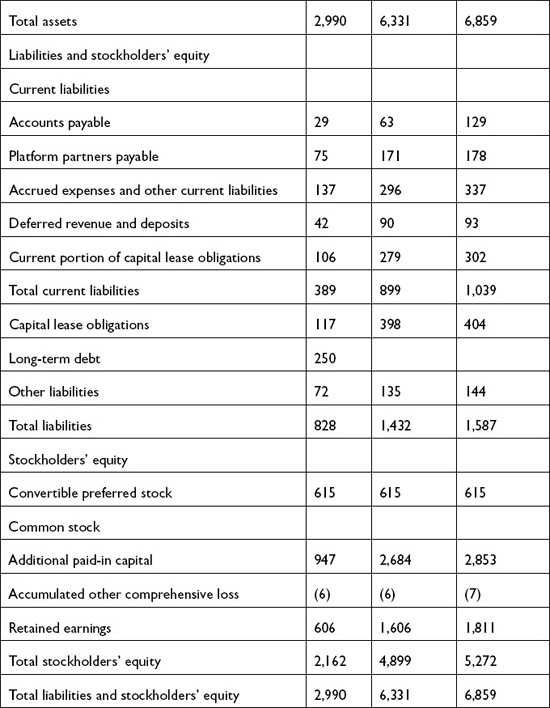

The balance sheet includes a company’s assets, liabilities, and equity. It should always balance according to this equation:

Assets = Liabilities + Equity

This makes intuitive sense because to buy assets, a company needs to raise capital by obtaining loans or selling stock. The equity also includes retained earnings, which are profits. It’s another key source for buying assets.

Tech companies like Facebook tend to be asset-light. Most of the value comes from supersmart engineers and the code they create—but they can’t be listed as assets on a balance sheet. Although Facebook has total assets of $7.1 billion, the company’s market value is over $50 billion.

Think of a balance sheet as a snapshot of a company at a certain point in time. It usually tallies everything at the end of the quarter, as you can see with Facebook’s balance sheet in

Table 8-2

.

Let’s take a look at the key items of the balance sheet.

An

asset

is anything a company owns, such as cash, inventory, or real estate. On a balance sheet, assets are listed in terms of

liquidity

, which is how quickly

they can be converted into cash. The current assets can be turned into cash within a year or so.

A large company like Facebook keeps a relatively small amount of its cash in deposits. Instead, it holds marketable securities, such as Treasuries. These are near-cash but pay somewhat higher yields. The yield can be a big deal for a company like Facebook, which has high cash balances.

An

account receivable

means a company has sold a product or service but the customer has yet to pay. This is actually an asset.

It’s possible for a company to factor or sell accounts receivable, which can be a source of cash. Doing so is common for early-stage companies, but it can be expensive because the fees tend to be steep.

Also keep in mind that a few customers simply fail to pay. It’s part of doing business (and it’s never fun to deal with). Because of this, a company estimates a total for these losses, which is called the

allowance for doubtful accounts

.

Prepaid assets

are those items for which a company makes advance purchases. To understand this, let’s take an example. Suppose Facebook prepays for five months of rent. It can recognize only one-fifth of this amount for the current month as an expense on the income statement. The rest is considered a prepaid asset.

According to GAAP, a company must depreciate property and equipment (but not land). This means it needs to reduce the value of the assets due to wear and tear and obsolescence.

A common approach is

straight-line depreciation

. This involves deducting an equal percentage periodically over the useful life of the asset. How long? It depends on the type of asset. This is what Facebook has:

- Network equipment:

3 to 4 years - Computer software and office equipment:

2 to 5 years - Buildings:

15 to 20 years

Let’s say Facebook buys network equipment for $100,000. If it uses a four-year term, then the depreciation is $25,000 per year.

A company may also use other depreciation methods that accelerate the process. These may take 25% or more of the value of the property in the first or second year. For the most part, these approaches are based on various tax incentives.

Goodwill

is the value from an acquisition: the purchase price minus the net asset value of the target company. Goodwill is fairly common in the tech world.

Suppose Facebook decides to pay $10 million for a mobile app company that has $1 million in net assets. The $9 million is accounted for as goodwill and considered an asset on the balance sheet.

To be in accordance with GAAP, goodwill must be tested at least once per year for

impairments

(this is the duty of an outside auditor). This is a fancy way of saying that an asset has lost value, such as from lower revenues or obsolescence. When there is an impairment, a company will need to take a loss.

A startup probably doesn’t have much debt. Banks generally avoid early-stage ventures because there is no collateral to lend against.

But there are still some liabilities. One form is

accounts payable

, which is money owed to vendors. As a company grows, so do these liabilities. It’s a key reason a startup needs to keep raising capital—and Facebook was no exception.

Cash is king. It definitely makes a founder’s life easier because it tends to mean much higher valuations and less pressure to raise outside capital.

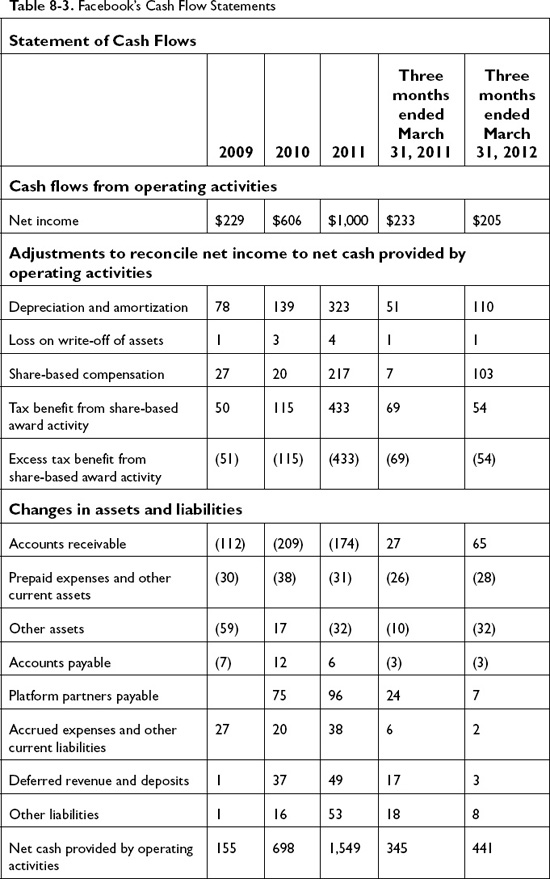

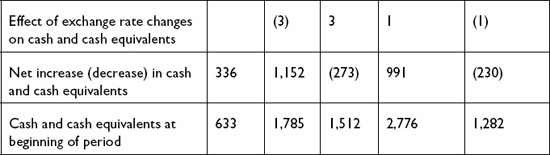

EBITDA is often used as a proxy for a company’s cash flows, but it’s a crude approximation. A better approach is to use the statement of cash flows.

Table 8-3

shows the statement for Facebook.

The statement includes adjustments for a variety of items on the income statement and balance sheet. Notice that there are three main sections, outlined next.

This shows Facebook’s cash flows from its operating business. The section begins with net income, which is then adjusted for a variety of items. This involves adding back non-cash amounts—such as depreciation, amortization, and share-based compensation—to the net income. Then other items must be subtracted. A key item is accounts receivable, because Facebook has yet to receive any cash.

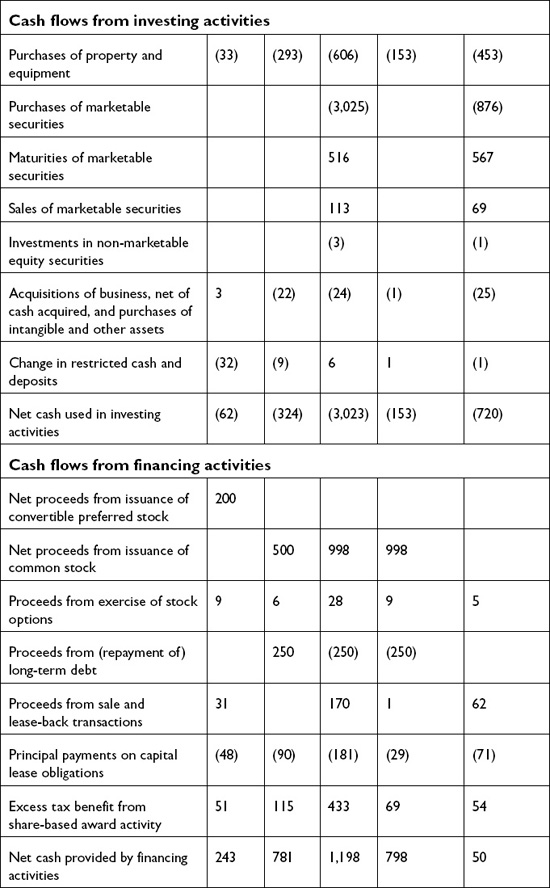

It’s common to confuse the Investing section with the Financing section. But they have clear differences.

The Investing section includes major purchases, usually capital expenditures for assets that should last longer than a year. But these purchases reduce cash flows. At the same time, any sales of assets increase cash flows.

Over the years, Facebook has substantially increased its investment in capital assets to allow for its strong growth.

This is where a company includes inflows from issuing stock and debt. Of course, any buybacks or dividends are subtracted.

For tech companies, the Financing section is a huge source of cash. But over time, the company needs to show that it can generate positive operating cash flows. If not, it’s a sign that the business model is flawed.

This chapter covered lots of ground and provided enough information for most entrepreneurs. Knowing the language and main concepts of accounting is a big help, not just for building credibility with VCs but also for running a successful business.

The next chapter continues the finance theme by looking at a company’s business model. There are many options to consider.

There seems to be some perverse human characteristic that likes to make easy things difficult.

—Warren Buffett

In Mark Zuckerberg’s letter to shareholders in February 2012, he made a brazen statement: “Facebook was not originally founded to be a company. We’ve always cared primarily about our social mission, the services we’re building and the people who use them.”

This is something you never hear from a public company’s CEO. They would be fired! Even Google—which considers itself to be unconventional—doesn’t have the same approach as Facebook.

According to Zuckerberg, “Simply put: we don’t build services to make money; we make money to build better services.”

Now that is unconventional. And it has worked extremely well. As you saw in the last chapter, Facebook has posted standout financials over the years.

For Zuckerberg, building social apps means avoiding the typical money-making aggressiveness that is prevalent in corporate America. Keep in mind that he could have easily plastered ads across Facebook, generating huge revenues. But Zuckerberg realized that this is the worst thing to do when creating an enduring company.

Just look at MySpace. From its origins, the company focused on monetizing—which became even more intense when News Corp. purchased the business. But it ultimately damaged the user experience and killed the company.

This chapter looks at strategies for pursuing a business model. You will first see how Facebook has done this and then examine other approaches that have proven to be successful as well.

The

business model

is how a company generates its revenues. When Facebook launched in 2004, the original vision was that it would focus on local ads. This made a lot of sense because the company was only in campus markets. As should be no surprise, there was a lot of demand for ads for local pizza joints and other cool hangouts. Classified ads were also popular because students moved frequently.

But as Facebook became ubiquitous, the business model evolved. As of now, it consists of two main sources of revenues: advertising and transaction fees from the Payments business.

Let’s first look at the advertising business, which is the main source of revenue (about 80% in 2011). Facebook has two main approaches. One is to use a direct sales force to sell to major companies and ad agencies. These engagements can take time to close and often require developing sophisticated campaigns.

Facebook also has a self-service ad platform, which allows any advertiser to use an online system to manage their own campaign. This is mostly for smaller companies that don’t have the budgets to hire advertising agencies.

Over the years, Facebook has invested heavily in developing systems for advertisers to get value from their advertising. The goal has been to demonstrate that there is a tangible return on investment (ROI).

Despite this effort, there have been concerns that social advertising is less effective than other approaches, such as Google-style search-engine marketing, television, and even radio. This was the conclusion of GM, which pulled all its Facebook advertising in May 2012. The belief was that the ROI was not compelling.

Perhaps one of the problems is that Facebook is a communications platform, which may not be optimal for serving ads because users are there to make comments, post status updates, and check out photos. Ads are often a distraction. It’s true that Facebook has put them in unobtrusive areas—but this makes the ads even less effective because they are easy to ignore.

Another problem is privacy. It seems inevitable that there will be more restrictions on the handling of user information, which is used for targeting for advertising. The big question is how far governments will go.

But Facebook has continued to improve its advertising system. Some of these efforts include the following:

- Targeting:

An advertiser can base ads on a group’s demographics. Factors include age, location, gender, relationship status, educational history, workplace, and interests. - Social context:

Advertisers can engage a user’s friends based on activities such as Liking the advertiser’s Facebook page. The idea is that people probably value a friend’s recommendations versus a straight ad. - Sponsored stories:

An advertiser can broadcast messages to more of its fans. - Analytics:

These track the performance of a campaign in real-time.

Although much of Facebook’s advertising revenue has come from the web site, this started to change rapidly in 2012. There was a major shift to mobile traffic, which caught Facebook off guard. It didn’t have the right infrastructure to monetize things, which resulted in a slowing of revenue growth. Traffic up, revenue down!

This was not the kind of message investors wanted to hear during the IPO in May and was a key reason for the lackluster reception. The good news is that Zuckerberg has declared mobile to be the company’s number-one priority.

But solving the problem will take time. Mobile advertising is still in the nascent stages, and advertisers are experimenting with approaches, trying to see which get the most ROI.

This is why entrepreneurs need to be temperate about a business model based on mobile traffic. It could take a few years to generate any meaningful revenue.

The other important takeaway is that any type of advertising business model requires lots of effort. You need to hire top people, including those who can create campaigns as well as salespeople who can land clients. You also need to build an infrastructure that effectively delivers and measures ad impressions. Such things are not cheap and should be a big part of any venture funding.

The Payments system allows Facebook partners to charge for their apps. It involves the secure processing of credit cards, PayPal transactions, gift cards, and other payment methods. Facebook gets a juicy 30% fee for all transactions.

In July 2011, Facebook began requiring that all social game operators use the Payments system, which resulted in a spike in revenues. The move was controversial with developers, but they understood the value of the platform.

Zynga accounts for much of the Payments revenues so far. But over time, this should change. Keep in mind that Facebook will likely get into other lucrative areas, such as allowing people to use their smartphones as wallets.

The temptation for entrepreneurs is to build their own payments system because doing so means more control over the process and improved customization of the user experience. But this approach is most likely to be a bad move. Payment systems are extremely expensive to create, requiring complex algorithms and security protocols. For most startups, the best approach is to outsource the function to a standout company like PayPal.

Back in early 2003, Mark Pincus started one of the first social networks, tribe.net. It got lots of traffic but was extremely difficult to monetize because it catered mostly to people with alternative lifestyles. Pincus experimented with different approaches, such as charging premium subscriptions, but nothing worked. He eventually sold the company to Cisco.

When it came to Pincus’s next venture, Zynga, he wanted to prove out the business model as soon as possible. He wondered if people would pay for digital items to advance to higher levels in a game. After a few tests, it was clear that some users definitely would do so, and this testing gave Pincus enough confidence to pursue his innovative business model.

But to make it a success, he needed to understand the main drivers. These became his laser focus.

With more experimentation and testing, Pincus realized that there were some key factors. Perhaps the most important was daily active users (DAUs). Growth in this metric had the highest correlation to revenue generation (this has also been the case with Facebook). Pincus focused heavily on finding ways to boost DAUs, such as aggressive advertising. He once said in a media interview that when he sees a person, he thinks of them as a DAU!

Pincus’ two-step process—to test the business model and find the drivers—is critical for any entrepreneur. Using a random approach is destined for failure, as seen with tribe.net.

From time to time, a company creates a game-changing business model. This was certainly the case with Google AdWords.

But it took several iterations to get it right. Google AdWords started as a simple way to buy text-based ads related to search results. They were separated from other search results and clearly described as advertisements. This allowed for a more authentic user experience.

AdWords did generate lots of revenues and was profitable, but the system was no different from any other Internet company. Simply put, advertisers would bid on common search phrases and the highest bids would get the best rankings. Then, a couple of years later, Google added a crucial twist: the auctions didn’t just rank ads on the amount of the bid but also factored in relevancy. The more clicks an ad got, the higher it was ranked. It was a huge breakthrough and resulted in explosive growth for Google: the ads were much more meaningful for users, which meant advertisers got high-quality leads.

But the company didn’t stop there. Google broadened the business model by also introducing AdSense, which allowed third-party web sites to host AdWords and get a piece of the revenue. It helped propel the business to amazing heights. Competitors like Yahoo! and AOL could not catch up.

Facebook is trying to invent innovative business models as well—but it knows that doing so is extremely tough. To help, the company has engaged in a great deal of experimentation. For example, in New Zealand it’s testing a new program called Highlight, which charges users to make posts to all their friends. It’s still in the early stages but will certainly gauge a user’s loyalty.

Business-model innovation may also come from acquisitions. Consider Facebook’s purchased of Karma in May 2012. The company is an early player in the gift-giving mobile app business. The idea is that Facebook can leverage its social graph to make it easier to recommend gifts to friends, which may result in a massive market for social commerce.

As is the nature of experimentation, many things fail, and Facebook’s experiments are no exception. Its Beacon advertising system, which was launched in 2007, was a total failure because people didn’t want their friends to see their online purchases. There was also a failed attempt to replicate a Groupon-type business.

Nevertheless, it’s worth the effort to be creative with your business model—and it should be an ongoing process. It can easily take a couple of years to refine the model.

But this is not to say that your business must innovate a business model. Many businesses do just fine using traditional approaches. The rest of the chapter looks at the primary ones.

This can be an extremely powerful business model. An example is eBay: it started as a way to sell Pez dispensers, but the platform proved versatile enough to sell virtually anything.

Even during the crazy dot-com era, eBay was one of the few companies that generated strong revenues and profits. The company didn’t need any outside cash but raised venture capital anyway so as to attract a top-notch executive like Meg Whitman.

Why are marketplaces great businesses? A key reason is that they allow members to generate extra income. With eBay, there are people who make thousands of dollars per month; some have made it their full-time business.

Over the past decade, other marketplaces have emerged. One of the most notable is Airbnb. At first, the company began as a way to rent someone’s couch to crash on! But the founders realized the business had much more potential: why not let people rent their apartments or homes to vacationers? It was a brilliant epiphany, and Airbnb turned into an instant hit, with huge revenues. The estimate is that the company will exceed $500 million in 2012.

Once a marketplace hits critical mass, it’s tough to dislodge. After more than 16 years, eBay is still the biggest player in online auctions. And it looks like this will remain the case for many years to come.

But there is something that can derail a marketplace: loss of trust. If users feel they may get ripped off, it can be a disaster. In the early days of eBay, the company had to deal with members who sold items and didn’t deliver them. As a result, the company took a variety of actions to reduce this activity. A key was implementing user ratings, which allowed for peer pressure.

Airbnb has had to deal with similar problems with user trust. In a couple of high-profile cases, members’ homes were trashed and valuable property was stolen. Airbnb took actions to deal with the issues, such as offering video verification systems and a personal property guarantee (up to $1 million). There is also a 24-hour customer-support line.

Entrepreneurs looking to create a marketplace need a lot of realism. It’s a proverbial chicken-and-egg dilemma: to get buyers, you need people to sell stuff; but to get sellers, you need buyers. The key for a successful marketplace

is to continually find the right balance, which takes a tremendous amount of effort and good timing.